Blogs

Video clips harbors took the online gambling community from the storm, as typically the most popular slot class certainly one of participants. With their interesting themes, immersive picture, and exciting extra has, these types of slots render endless entertainment. They’lso are perfect for those who take pleasure in free slots enjoyment having a nostalgic reach. While they may not boast the fresh flashy graphics of modern movies harbors, vintage harbors provide an absolute, unadulterated playing feel.

The game is cellular enhanced and are available for the smartphone products. You don’t have far to love the brand new thrill from to try out harbors on the web. You will find various 100 percent free https://happy-gambler.com/slots-heaven-casino/20-free-spins/ trial ports in order to play immediately for the our website no download required. All of our program offers a person-friendly software, to make navigating and you will searching for a favourite slots effortless.

The brand new Canadian gambling establishment provides reveal FAQ to let people to help you resolve the queries quickly. At the same time, the new operator also offers an intensive assist cardiovascular system. The platform will bring comprehensive choices about your account, purchases, bonuses, alive gambling establishment, sportsbook, and you may online game regulations. Whether your play Sweet Bonanza or Doors out of Olympus, all online game are cellular-optimized to include simple gameplay. Though there’s no Leo Las vegas Casino download for Pc, you could potentially play on your web internet browser. You’ll notice it simpler playing Leo Vegas instantaneous, that have very little lags.

Leo Vegas Local casino Ontario Opinion

- Antique harbors are the cornerstone of any Vegas gambling enterprise, as well as their on line counterparts are no other.

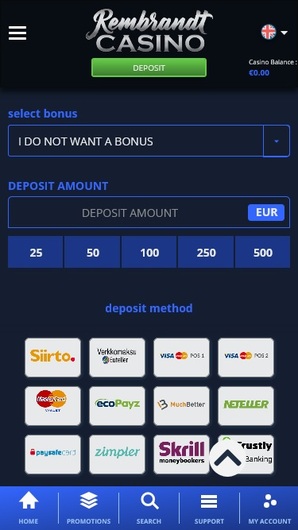

- Instadebit, at the same time, will set you back California$step one.fifty to place in initial deposit.

- Anyone who could have been to Las vegas for the past few many years cannot features assisted observe that the fresh Small Strike slots are increasingly being a little more about common with each and each seasons you to passes.

- You’ll need around three or more scattered Bonus signs so you can cause the fresh Keep & Winnings Function that have three respins.

- If the there are one terminology you’re not knowing of otherwise bonus provides you would want to understand, head right down to our very own glossary section.

- You can also get touching the new gambling establishment because of the chatting with otherwise getting in touch with their British or Global help cell phone numbers.

The brand new big video game list from the Leo Las vegas try presented by many people of one’s industry’s best software team. You will find live online casino games from the Evolution, Pragmatic Gamble Live, and you can Playtech, and others. Different themed slots are created from the large and small labels, along with ELK Studios, Play’n Wade, Calm down Gaming, Pragmatic Gamble and much more. Even the customer let team via alive chat wouldn’t divulge this article in order to all of us, that was among the only downfalls while in the all of our review of this gambling establishment. The fresh alive broker casino is where Leo Vegas extremely stands out, holding the greatest band of live dealer gambling establishment application of any online area.

A few of the options for deposits try immediate, so that you will be able to wager immediately. We have been a slot machines ratings site for the a goal to provide participants with a trusting supply of gambling on line advice. We exercise through unbiased ratings of your own harbors and you may casinos we gamble in the, continued to incorporate the fresh harbors and maintain you up-to-date on the newest ports information. There is also an excellent list of table online game along with 38 roulette distinctions as well as 52 cards. That it, combined with its sophisticated live dealer casino, can make Leo Las vegas probably one of the most complete the newest casino websites to experience to the entire net.

Amazingly, the easy step 3-reel game are already still well-known. Possibly considering the ease, or even the hypnotic music that they generate, and/or the fact that they think ‘real’, because if they nonetheless got mechanical reels spinning. IGT, the guys whom build Sex as well as the Town Ports and Wolf Work with supply video game to have British participants. In the uk, most of the IGT games are labeled less than their Barcrest name, however, more frequently, the new IGT image is revealed more any other.

- Perhaps the customer assist group via real time chat won’t disclose this informative article to help you all of us, which had been one of several only downfalls throughout the our very own review associated with the local casino.

- These businesses that provide LeoVegas gambling software solutions is highly rated.

- The organization considering LeoVegas within the Canada for several years prior to Ontario brought an in your area controlled field.

Do you know the finest totally free slots?

Perhaps one of the most wonderful things about Buffalo Slots is the fact all variation they make are practical yet the first has been great fun to try out. Instead of most other slots, with las vegas Community you can actually keep in touch with most other players and you may connect to them. Including, you can visit a celebration and now have a dance that have most other people. You can also find your own Las vegas apartment and modify it as your progress from the game. When Siberian Storm was first put-out on the casinos, it was a simple strike.

Better Mobile Casinos Playing Harbors

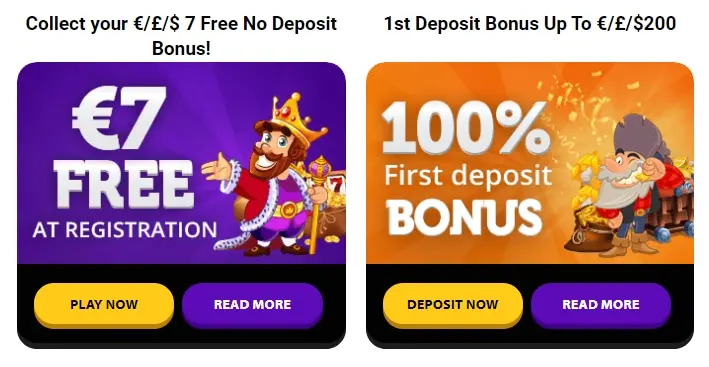

Jackpot slots can offer the biggest win potential of every position game. It’s as to the reasons of a lot players continue to head to those games to own a way to win. Several of the most played jackpots at that gambling establishment is Mega Moolah, Absolootely Angry Mega Moolah and you may Queen out of Alexandria WowPot. Simply create a genuine money put of $ten or more, and LeoVegas often suits it from the one hundred% as much as $a hundred. Keep in mind that deposits generated having fun with Neteller or Skrill aren’t qualified to the real time agent added bonus. You ought to claim the advantage in this 1 week away from registering an enthusiastic membership during the website.

Which have Slot Tracker, you can view research and analytics on the people casino your play from the, not merely LeoVegas. The newest creator are expected to provide privacy facts when they complete their 2nd app inform. They are able to also be hit via age-mail and cellular telephone and they’ve got probably one of the most comprehensive FAQ parts around. Leo Las vegas is very easy to reach and so they most wade out of their solution to care for their clients within the any kind of capability they require.

Sweepstakes Public Gambling enterprises

Area of the emphasize of one’s position is actually Kalamba’s K-Dollars function, that helps you gather free spins and K-Cash multiplier thinking to have increased profits. We’re going to always like free Vegas penny slots, but we along with trust the new gambling games are entitled to a shout out. LeoVegas as well as operates a thorough help and FAQ point, you will be able to availability those options as well and find a way to people clicking amount or relaxed query. LeoVegas means that it includes you which have answers twenty four/7 within their impeccable dedication to players. The individuals kinds tend to be Greatest Games, Newest Online game, Need to Slip Jackpots, Jackpots, Slots, Table Online game, and you will Bingo.

The new gambling games are enhanced to add an intuitive playing experience, since the Dark Function feature try a plus to own professionals. If this is a downside for your requirements, choose almost every other greatest zero-account gambling enterprises. Wolf Gold by Pragmatic Gamble try a character-styled on the web slot having a captivating journey from wasteland. That have 5 reels and you will twenty five pay lines, there are many chances to property winning combos. The online game also offers an enthusiastic RTP of 96%, making certain a good playing feel. Immerse yourself within the an organic community as you run into majestic wolves or other wildlife icons.

See Your favorite Position Layouts

Local casino fans in the us are now able to play during the Sweepstakes Personal Gambling enterprises. You could potentially wager totally free in the a good sweepstakes casino nevertheless can earn honours, even with no purchase. Or you can pick a package / give for more gold coins to suit your currency, and more chances to earn.

For this reason, you could potentially sit in hopes you to, discussing this provider, you’ll maximize enjoyable sense. For certain, you won’t ever find some other average net gambling enterprises to suit the newest experience that you’ll build, referring to that it people. Furthermore, online gambling concerns investing delicate analysis between gambling enterprises and players. Mismanagement could help hackers gain command over the bank account. In addition your own address and you may ID number are on the line. Luckily, LeoVegas transmits and areas analysis for the TLS step 1.step three, a premier-fundamental encryption process for banking institutions.

Leo Las vegas have more 30 progressive harbors that have honours within the the newest several millions. A current winnings on the a modern position netted one lucky gamer a £cuatro.cuatro million jackpot. The fresh legendary Swedish hockey athlete offered to portray the fresh agent while the an ambassador and you will collaborator. Mats try the leading deal with regarding the hockey world with a long set of success, along with multiple world championships, Olympic Silver Medalist, and Hockey Hallway from Glory subscription. The brand new approval considering advanced applicants away from a marketing view so you can fortify the new platform’s condition and sustain strong growth in Canada. When you are email address assistance features a fast recovery with fast responses, the new twenty four/7 alive talk service is another extremely important feature of your assistance staff.